You are sitting with a pile of rent receipts on a Tuesday afternoon. An employee walks into your cabin and asks why his Form 16 last year showed a smaller HRA exemption than he expected. You open the calculation, and three minutes in, you are explaining 50% versus 40%, what counts as “salary”, and why his Pune apartment did not get the metro rate.

That conversation is about to change. From 1 April 2026, the rules around House Rent Allowance have shifted in ways that affect how every HR team in India calculates, documents, and reports HRA. Here is the practical guide your payroll desk needs.

TL;DR — HRA Exemption 2026 in 30 Seconds

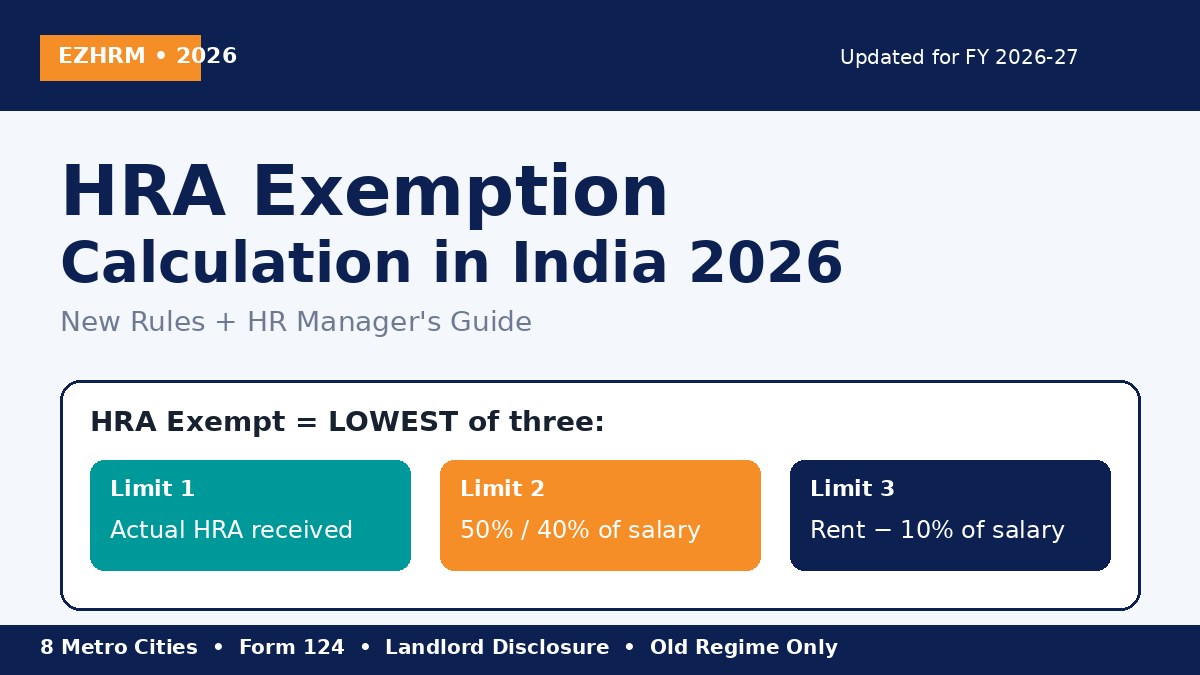

- HRA exemption under Section 10(13A) is the lowest of three values: actual HRA received, 50%/40% of salary, or rent paid minus 10% of salary.

- From FY 2026-27, Bengaluru, Pune, Hyderabad and Ahmedabad join Delhi, Mumbai, Kolkata and Chennai as 50% metro cities — eight metros now.

- Form 12BB is replaced by Form 124 from 1 April 2026, with mandatory landlord-relationship disclosure.

- HRA is only available under the Old Tax Regime — and the New Regime is the default unless your employee opts out in writing.

What is HRA Exemption Under Section 10(13A)?

House Rent Allowance is a salary component employers pay to help cover an employee’s rent. Section 10(13A) of the Income Tax Act, read with Rule 2A, lets a salaried employee claim part of that HRA as tax-exempt — provided they actually live in rented accommodation and meet the conditions.

This is not a flat percentage. It is the least of three calculations, and that is where most HR teams trip up. Get the formula wrong, and you either short-change the employee on Form 16 or set up a notice from the assessing officer at ITR time.

HRA Exemption Formula (Updated for 2026)

For each financial year, calculate three numbers. The exempt HRA is the smallest of them.

| Limit | What to Calculate |

|---|---|

| Limit 1 | Actual HRA received from the employer in the year |

| Limit 2 | 50% of salary if employee lives in a metro; 40% of salary for non-metro |

| Limit 3 | Rent actually paid in the year minus 10% of salary |

“Salary” here means Basic + Dearness Allowance (the part forming retirement benefits) + commission as a fixed % of turnover. Nothing else. Special allowance, HRA itself, performance bonus, LTA — all excluded from the salary base.

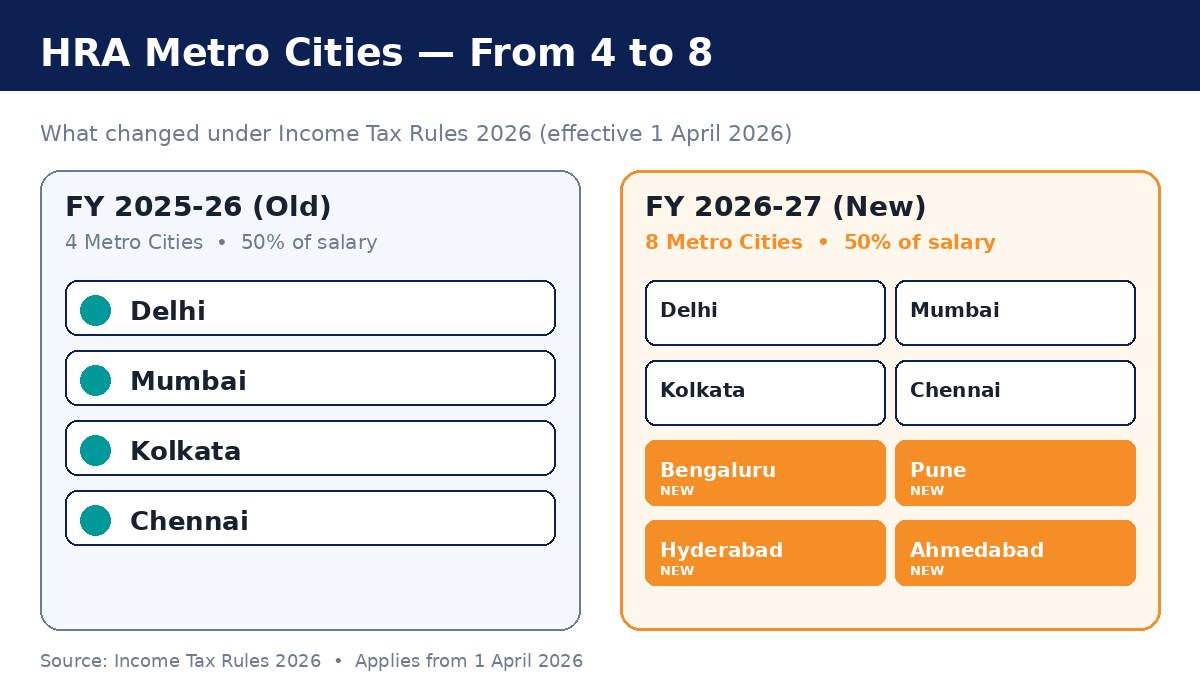

What Changed: The Metro List Doubled

Until FY 2025-26, only four cities counted as metros for HRA purposes: Delhi, Mumbai, Kolkata, Chennai. A Bangalore engineer paying ₹35,000 rent on the same salary as a Mumbai colleague got a smaller exemption — purely because of city classification.

From FY 2026-27, the Income Tax Rules 2026 add four more cities to the 50% bucket: Bengaluru, Pune, Hyderabad and Ahmedabad.

If your team has staff in any of these four cities, their HRA exemption ceiling jumps from 40% to 50% of salary starting 1 April 2026. For an employee with ₹50,000 basic, that is up to ₹5,000 a month of additional shielded income.

One thing to note: For FY 2025-26 (the ITR your employees will file by 31 July 2026), the old 4-metro rule still applies. The expanded 8-city list is for FY 2026-27 onwards. Do not apply the new list retrospectively when finalising Form 16 for FY 2025-26.

Worked Example: Ramesh in Bengaluru, FY 2026-27

Ramesh is your team lead in your Bengaluru office. His monthly numbers:

- Basic: ₹50,000

- DA: Nil (private firm, no DA)

- HRA received: ₹25,000

- Rent paid: ₹30,000

Annualise everything. Salary for HRA = ₹50,000 × 12 = ₹6,00,000.

| Limit | Calculation | Amount |

|---|---|---|

| Limit 1 | Actual HRA (₹25,000 × 12) | ₹3,00,000 |

| Limit 2 | 50% of ₹6,00,000 (Bengaluru is now metro) | ₹3,00,000 |

| Limit 3 | (₹30,000 × 12) − 10% of ₹6,00,000 = ₹3,60,000 − ₹60,000 | ₹3,00,000 |

Exempt HRA = the lowest of the three = ₹3,00,000.

Under the old 40% rule, Limit 2 would have been ₹2,40,000, dropping his exemption to ₹2,40,000. Ramesh saves tax on ₹60,000 of additional income this year — purely because of the new metro classification.

Form 124 + 2026 Documentation Checklist

Every payroll team has been collecting Form 12BB at the start of the year. From 1 April 2026, Form 124 takes its place. Form 124 asks for everything 12BB did, plus three new items:

- Landlord’s full name and complete address

- Landlord’s PAN (if rent exceeds ₹1,00,000 in the year — same threshold as before)

- Employee’s relationship with the landlord (new mandatory disclosure)

- Mode of rent payment

That last item is the one that changes how you process rent claims paid to parents or spouses. The relationship has to be declared up front. The Income Tax department wants to clean up cases where employees pay “rent” on paper to family members who are not actually receiving it.

HRA Documents Checklist for FY 2026-27

- Rent receipts for every month rent was paid (mandatory if monthly rent > ₹3,000)

- Rental agreement on stamp paper (recommended even when not legally mandatory)

- Landlord’s PAN copy (compulsory if annual rent > ₹1,00,000)

- Landlord-relationship disclosure on Form 124

- Bank statement or UPI transaction proof showing rent transfers

- Salary structure showing HRA is a defined component of CTC

If rent is paid in cash, ask for a stamped receipt and a written explanation. Cash rent is not banned, but it draws scrutiny. Where the trail looks weak, the assessing officer can disallow the claim.

Old vs New Tax Regime — and the Family Rent Rule

This is where most queries land in the HR inbox.

| Tax Regime | Can Employee Claim HRA? |

|---|---|

| Old Tax Regime | Yes — full Section 10(13A) benefit |

| New Tax Regime | No — HRA exemption not available |

Since the New Tax Regime is the default from FY 2023-24, your employee has to actively opt for the Old Regime to claim HRA. Capture this preference in writing — ideally in the same Form 124 declaration — and process payroll TDS accordingly. If an employee opts for the Old Regime mid-year, your payroll software needs to reconcile TDS already deducted under the New Regime. This is one of those moments where Excel breaks down and a proper HRMS earns its fee.

Paying Rent to Family in 2026: What is Different

Paying rent to your parents or spouse is legal, and HRA can still be claimed — but the new rules tighten the file you need to keep.

- Rent must actually be paid — banking channel preferred (UPI, NEFT, IMPS, cheque)

- The landlord must declare the rental income in their own ITR

- The relationship must be disclosed on Form 124

- A registered or notarised rent agreement is strongly recommended

- The arrangement must be at a fair market rent, not inflated

Section 439 of the Income Tax Act, 2025 brings a sharper penalty regime — up to 200% of the tax sought to be evaded for misreporting. Tell your employees plainly: do not fudge family-rent claims to save tax. The paperwork has caught up.

Common Mistakes HR Managers Get Wrong

Six errors I see every appraisal cycle:

- Using gross salary, not Basic + DA. HRA salary is narrow — Basic + DA forming part of retirement benefits + commission as % of turnover. Allowances, bonuses, special pay are all excluded.

- Treating Bengaluru or Pune as non-metro for FY 2026-27. From this April, they are 50% cities along with Hyderabad and Ahmedabad.

- Skipping landlord PAN when annual rent crosses ₹1,00,000. The Income Tax department cross-matches PANs. A missing PAN can disallow the entire exemption.

- Letting employees claim HRA under the New Regime. Your TDS calculation will not budge — but the employee will end up confused at ITR filing time.

- Accepting handwritten receipts only. Pair receipts with bank-transfer proof. The trail matters more than the receipt.

- Forgetting to update Form 12BB → Form 124 in your onboarding kit and investment-declaration cycle. A small but real compliance miss for FY 2026-27.

If you want a structured run-through of investment declarations for the new financial year, our Investment Declaration FY 2026-27 checklist pairs neatly with this guide.

HRA Exemption FAQs

Q1. Can an employee claim HRA if they live in their own house?

No. HRA exemption under Section 10(13A) is allowed only when the employee actually pays rent for the accommodation they live in. If they own and live in the house, the exemption is zero — even if HRA is part of their CTC. They can still claim home-loan benefits separately under Sections 24(b) and 80C in the Old Regime.

Q2. Is HRA exemption available under the New Tax Regime in 2026?

No. HRA exemption under Section 10(13A) is not available in the New Tax Regime. Since the New Regime is the default, employees who want to claim HRA must explicitly opt for the Old Regime in their Form 124 declaration to the employer at the start of the financial year.

Q3. Do I need landlord PAN for every employee claiming HRA?

Only if the employee’s annual rent exceeds ₹1,00,000. For smaller amounts, rent receipts and a rent agreement are sufficient. Where rent crosses ₹50,000 a month, the employee must also deduct TDS at 2% under Section 194-IB and deposit it — separate from the HRA documentation flow you handle as employer.

Q4. From when does the new 8-metro HRA rule apply?

From 1 April 2026 — meaning FY 2026-27 onwards. For FY 2025-26 (current ITR filings due 31 July 2026), the old 4-city list (Delhi, Mumbai, Kolkata, Chennai) still applies. Do not apply the new list retrospectively when computing Form 16 for FY 2025-26.

Q5. Can an employee pay rent to their spouse and claim HRA?

Yes, but with full compliance: bank-channel rent payment, registered rent agreement, declaration on Form 124, the spouse declaring the rental income in their ITR, and a reasonable fair-market rent. The relationship must be disclosed. Misreporting can attract penalties up to 200% of tax evaded under Section 439 of the Income Tax Act, 2025.

Q6. What if an employee changes city mid-year?

Calculate HRA exemption separately for each period. If they moved from a non-metro to a metro in October, use 40% for April–September and 50% for October–March against the relevant salary and rent for each period. Most modern HRMS platforms handle this split automatically; manual Excel sheets often miss the proration.

Getting HRA right month after month — across regions, regimes, and the new Form 124 rules — is exactly the work that drains a payroll team. EZHRM’s TDS & Form 16 module handles HRA exemption calculation, Form 124 collection, landlord PAN tracking and Form 16 generation in one flow, so your team stops chasing receipts every March.