It’s May. Your CFO has just asked, “What’s our bonus liability for FY 2025-26?” — and you’re staring at a spreadsheet wondering which of your 84 employees actually qualify, what the right calculation base is, and whether the ₹21,000 ceiling still applies in 2026. If you’ve ever fudged through this question, this guide is for you.

Statutory bonus is one of those compliances HR teams in Indian SMEs treat as a Diwali-time scramble. Done well, it’s a painless 30-minute exercise per cycle. Done poorly, it lands you with Section 28 prosecution, 9% interest, and an annoyed labour inspector.

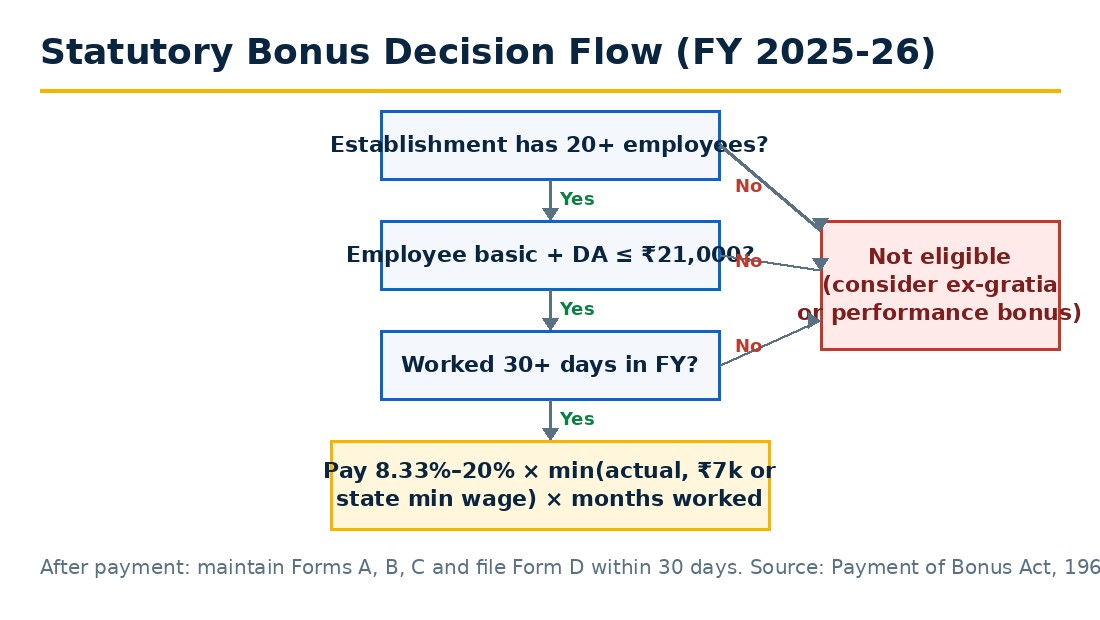

- Statutory bonus under the Payment of Bonus Act, 1965 applies to any establishment with 20+ employees (or any factory, regardless of count).

- An employee qualifies if their basic + DA is ≤ ₹21,000/month and they’ve worked 30+ days in the financial year.

- Bonus = 8.33% to 20% of (basic + DA), capped at ₹7,000/month or the state minimum wage, whichever is higher.

- Bonus for FY 2025-26 must be paid by 30 November 2026; Form D is filed within 30 days of payment.

What Is Statutory Bonus in India?

Statutory bonus is a legally mandated payment Indian employers owe to lower-wage employees under the Payment of Bonus Act, 1965. Unlike a performance bonus or an ex-gratia Diwali gift, it is not discretionary. If your establishment qualifies and the employee qualifies, the cheque must be written — even in a year your business made a loss.

The minimum bonus is 8.33% of the eligible wage and the maximum is 20%. The percentage between those two depends on a calculation called “allocable surplus” (more on that in a minute).

Who Has to Pay Statutory Bonus?

The Act applies to two categories of employers:

- Every factory as defined under the Factories Act, 1948 (regardless of headcount).

- Every other establishment with 20 or more employees on any day during the accounting year.

Once the 20-employee threshold is crossed, the obligation continues even if your headcount drops below 20 in subsequent years. State governments can also extend the Act to establishments with as few as 10 employees through specific notifications, so check your state’s Shops & Establishments rules.

Who Is Exempt?

Most newer companies get a 5-year exemption — but with a catch. A new establishment is not required to pay bonus until it makes profit, and only from the accounting year in which it first earns profit. Once profitable, the bonus obligation begins from that year. After the first 5 years are up, the obligation is unconditional.

LIC, RBI, government employees, employees of educational institutions, hospitals, social welfare institutions, and Red Cross are also outside the Act’s scope.

Which Employees Qualify?

An employee is entitled to bonus if they meet both of these conditions:

- Their basic + DA is ₹21,000 or less per month (other allowances like HRA, conveyance, special allowance are excluded from this test).

- They’ve worked at least 30 days in the relevant accounting year.

That’s it. You don’t need to look at designation, contract type, or whether they’re permanent or fixed-term. If a contract worker, apprentice (under your payroll, not under the Apprentices Act), or part-timer hits these two thresholds, they’re in.

An employee who is dismissed for fraud, riotous behaviour, or theft from the employer’s property is disqualified — this is the only conduct-based exclusion.

How to Calculate Statutory Bonus in 2026

This is where most HR managers get confused. There are two ceilings working together — the eligibility ceiling (₹21,000) and the calculation ceiling (₹7,000 or state minimum wage). Don’t conflate them.

The bonus formula is:

Bonus = Bonus % × (Basic + DA, capped at ₹7,000/month or state minimum wage, whichever is higher) × Months worked

Worked Examples

| Employee | Basic + DA / month | State Minimum Wage | Calc Base / month | Min Bonus (8.33% × 12) | Max Bonus (20% × 12) |

|---|---|---|---|---|---|

| Priya (HR Exec) | ₹15,000 | ₹10,500 | ₹15,000 (actual ≤ ₹21k, so use actual capped at ₹7k floor / min wage. Min wage ₹10,500 > ₹7k, so cap = ₹10,500) | ₹10,495 | ₹25,200 |

| Ramesh (Operator) | ₹9,000 | ₹10,500 | ₹9,000 (actual is below state min wage, so we use ₹9,000 — cap doesn’t apply since it’s the floor we measure against) | ₹8,996 | ₹21,600 |

| Sunita (Helper, Haryana) | ₹14,000 | ₹11,200 | ₹11,200 (cap applies since actual > cap) | ₹11,194 | ₹26,880 |

| Anil (Sr Engineer) | ₹28,000 | — | Not eligible (basic + DA > ₹21,000) | — | — |

The trick: the calculation cap is the higher of ₹7,000 or the state minimum wage for the lowest scheduled employment grade. In most states (Haryana, Delhi, Maharashtra, Karnataka), minimum wage already exceeds ₹7,000, so the state figure governs.

Allocable Surplus and the Set-On / Set-Off Rule

The 8.33%-to-20% range is decided by your “allocable surplus” — broadly, 60% of available surplus (67% for companies that don’t pay dividends abroad). If allocable surplus per eligible employee is below the 8.33% floor, you still pay 8.33%. If it’s above 20%, you pay 20% and “set on” the excess (carry forward) for up to 4 years. In a loss year, you can “set off” prior set-on amounts to reduce future obligations — but never below the 8.33% minimum.

Statutory Bonus vs Ex-Gratia vs Performance Bonus

| Type | Mandatory? | Eligibility | Calculation | Forms |

|---|---|---|---|---|

| Statutory Bonus | Yes (under Bonus Act) | Basic + DA ≤ ₹21,000, 30+ days worked | 8.33%–20% of capped wage | A, B, C, D |

| Ex-Gratia | No (employer’s discretion) | Anyone — typically those above ₹21,000 | Flat amount or % decided by management | None |

| Performance Bonus | Per contract | As per appointment letter / policy | Linked to KRAs or company performance | None statutory |

A common pattern: pay statutory bonus to those below ₹21,000 and ex-gratia (often labelled “Diwali bonus”) to senior staff. Just don’t call ex-gratia “statutory bonus” in your payslip — it confuses tax treatment and audit trails.

Forms A, B, C and D: What HR Must File

The Bonus Rules, 1975 require four registers and a return:

- Form A — Computation of allocable surplus (kept on file).

- Form B — Set-on and set-off of allocable surplus (running register).

- Form C — Employee-wise details of bonus paid (date, amount, deductions).

- Form D — Annual return to the Inspector under the Act, filed within 30 days of bonus payment.

Forms A, B, and C are internal records you must produce on inspection. Form D goes to the labour office (some states now accept it via Shram Suvidha or the state labour portal). Keep digital and physical copies for 8 years — that’s the inspection look-back window most labour officers use.

Key Dates for FY 2025-26 Bonus

- 30 November 2026 — Last date to pay statutory bonus (8 months from FY-end).

- Within 30 days of payment — File Form D.

- Most companies pay before Diwali (October–November) for cultural reasons; this is fine as long as it’s before 30 Nov.

Common Mistakes HR Managers Make

After running through hundreds of audits, the same five errors keep showing up:

- Calculating on gross salary, not basic + DA. If you pay 8.33% of someone’s ₹35,000 CTC, you’re paying nearly 4× the legal requirement. Use basic + DA only, capped at ₹7,000 / min wage.

- Forgetting the floor on a loss year. “We made a loss, so no bonus” is wrong. Statutory minimum is 8.33% — even if your P&L shows red.

- Skipping Form D filing. Most SMEs pay bonus diligently and then never file Form D. The penalty (Section 28: up to 6 months imprisonment or ₹1,000 fine) is rarely enforced, but it’s the first thing labour officers check.

- Treating bonus as taxable in the wrong year. Statutory bonus is taxable in the year of payment, not the year it relates to. Reflect it in payroll TDS in the month you actually pay it.

- Excluding contract workers on principle. If a contract employee meets both conditions and is on your direct payroll (not via a third-party contractor), they are eligible. Many companies miss this and face claims later.

Penalties for Non-Payment or Late Filing

Section 28 of the Act prescribes imprisonment up to 6 months, a fine up to ₹1,000, or both. In practice, what hurts more is:

- Interest at 9% per annum on unpaid bonus from the due date until payment.

- Recovery as arrears of land revenue by the labour officer.

- A poor record on the Shram Suvidha portal — which now flags repeat defaulters during inspections of other compliance areas like PF and ESI.

Frequently Asked Questions

Is statutory bonus the same as Diwali bonus?

No. Diwali bonus is a cultural or ex-gratia payment most Indian employers make voluntarily around the festive season. Statutory bonus is a legal obligation under the Payment of Bonus Act, 1965, with specific eligibility, calculation, and filing rules. You can pay both, but only the statutory portion attracts the Act’s penalties if missed.

Can I pay statutory bonus monthly instead of annually?

Yes. Some employers split the annual bonus into 12 equal monthly payments to ease cash flow. This is allowed as long as the total annual amount is not less than 8.33% of eligible wages and you maintain records under Forms A, B, and C. Mention it explicitly in the appointment letter to avoid confusion.

What happens if my company has fewer than 20 employees?

You are not covered under the Bonus Act unless your state has notified a lower threshold (some states have extended it to 10 employees) or your business is a factory. However, once you cross 20 employees on any day during a financial year, the obligation kicks in for that year and continues even if headcount later falls.

Are interns and apprentices eligible for bonus?

Apprentices engaged under the Apprentices Act, 1961 are excluded from the definition of “employee” under the Bonus Act. Interns and trainees on your direct payroll are eligible if they meet the ₹21,000 wage cap and 30-day work test. Call out their status clearly in offer letters.

Does the new Code on Wages, 2019 change the bonus rules?

The Code on Wages, 2019 retains the bonus framework largely as-is but consolidates it with three other wage-related laws. Until the Code is notified across all states (still pending in 2026), the existing Payment of Bonus Act, 1965 continues to apply. Watch for state-level notifications.

Can bonus be deducted from salary or adjusted against advances?

Section 18 of the Act allows adjustment only in two cases: bonus already paid as interim or puja bonus during the year, and money owed to the employer due to misconduct that caused financial loss. Routine salary advances or notice-period dues cannot be set off against statutory bonus.

Stop Tracking Bonus on Spreadsheets

Bonus calculation is one of those compliance items that look