Every November, without fail, someone on your team will ask: “How much bonus am I getting this year?” And somewhere in the same week, at least one business owner will quietly ask you whether the company can “skip it” this year. It cannot. Statutory bonus under the Payment of Bonus Act, 1965 is not a Diwali gift or a performance reward — it is a legal obligation. Miscalculate it, or miss the November 30 deadline, and your company is looking at penalties, labour inspector visits, and very unhappy employees.

This guide walks you through the exact formula, the eligibility rules, the filing requirements, and the most common mistakes Indian HR managers make — so you can get it right the first time, every time.

TL;DR: Statutory Bonus 2026 at a Glance

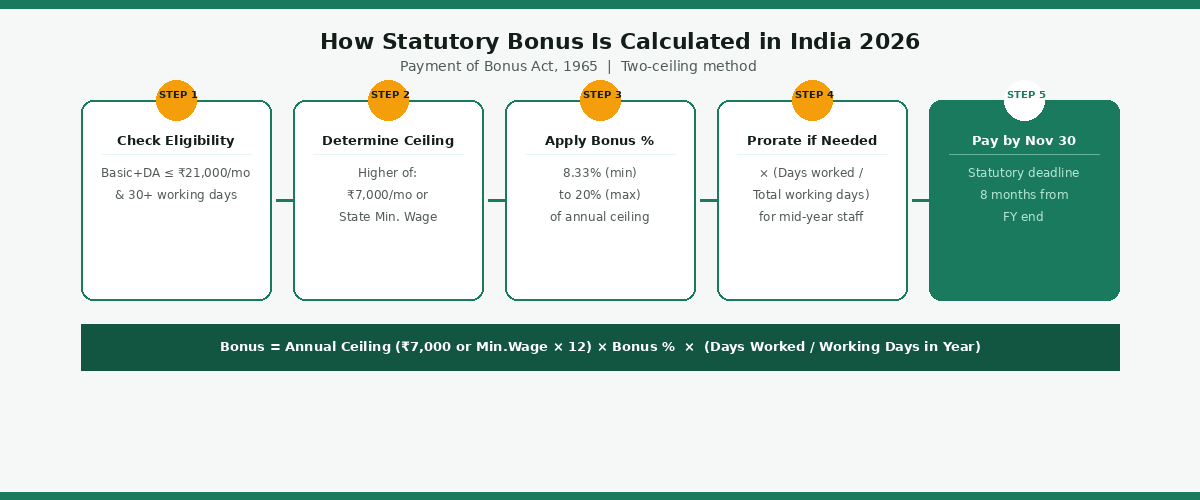

Eligible employees: drawing Rs. 21,000/month (Basic + DA) and who worked 30+ working days in the accounting year. Minimum bonus: 8.33% of salary; maximum: 20% — calculated on Rs. 7,000/month or applicable minimum wage, whichever is higher. Payment deadline: 30 November 2026. Use the free EZHRM Statutory Bonus Calculator to get employee-wise figures instantly.

What Is Statutory Bonus Under the Payment of Bonus Act, 1965?

Statutory bonus is a mandatory annual payment that every employer covered under the Payment of Bonus Act, 1965 must make to eligible employees. It is not discretionary, not linked to individual performance, and cannot be replaced or offset by a “festival bonus” or any other ex-gratia payment unless explicitly declared as such in writing.

The Act applies to every factory (as defined under the Factories Act, 1948) and every other establishment in which 20 or more persons are employed on any day during an accounting year. Once an establishment crosses the 20-employee mark, it remains covered even if its headcount later falls below that number.

The accounting year under the Act runs from 1 April to 31 March — aligned with the Indian financial year. Bonus must be paid within 8 months of the close of the accounting year, which means the deadline for FY 2025-26 is 30 November 2026.

Who Is Eligible for Statutory Bonus in India 2026?

Three conditions must all be met for an employee to be entitled to statutory bonus:

1. Salary Ceiling: Rs. 21,000 per month

Only employees whose salary (Basic + Dearness Allowance) does not exceed Rs. 21,000 per month are eligible. This ceiling was revised from Rs. 10,000 to Rs. 21,000 by the Payment of Bonus (Amendment) Act, 2015, which came into effect retrospectively from 1 April 2014. Employees earning above Rs. 21,000 per month in Basic + DA are entirely excluded — even if their take-home CTC is close to that figure.

Note: HRA, conveyance, and other allowances beyond Basic and DA are not counted for this ceiling. To understand how these components fit into an overall salary structure, use the EZHRM CTC Salary Calculator.

2. Minimum Service: 30 Working Days

The employee must have worked at least 30 working days in the accounting year. Days of leave (paid or unpaid), lay-off, maternity leave, and legal strikes count as “working days” under the Act. An employee who joins in March and works only 25 days is not eligible for that year’s bonus.

3. Establishment Size: 20+ Employees

The establishment must have employed 20 or more persons on any day during the accounting year. This is a one-time trigger — once crossed, the Act applies permanently regardless of subsequent headcount changes.

Who Is Excluded?

The Act explicitly excludes employees of the Life Insurance Corporation of India, seamen, dock workers under a separate scheme, employees of universities and educational institutions, and employees of certain government departments. Check the full exclusions list under Section 32 of the Act if you are in a specialised sector.

How to Calculate Statutory Bonus: The Exact Formula

The statutory bonus calculation formula uses two separate salary limits. The eligibility ceiling is Rs. 21,000/month (Section 2(13)). The calculation ceiling is Rs. 7,000/month or the minimum wage notified by the government for the lowest grade of employee in your industry/state, whichever is higher (Section 12).

Formula: Statutory Bonus = Annual Calculation Ceiling x Bonus % x (Working Days / Total Working Days in Year)

In simpler terms: even if an employee earns Rs. 18,000/month, you do not calculate bonus on Rs. 18,000. You calculate it on Rs. 7,000 (or the applicable minimum wage if higher). This is where most HR managers silently underpay.

Worked Example — Minimum Bonus at 8.33%

| Detail | Employee A | Employee B |

|---|---|---|

| Basic + DA per month | Rs. 9,000 | Rs. 19,500 |

| Eligible (Rs. 21,000 ceiling)? | Yes | Yes |

| Calculation base (Rs. 7,000 or min. wage — whichever higher) | Rs. 7,000 | Rs. 7,000 |

| Annual calculation base (x 12) | Rs. 84,000 | Rs. 84,000 |

| Bonus % applied | 8.33% | 8.33% |

| Minimum Bonus Payable | Rs. 6,997 | Rs. 6,997 |

Notice something? Both employees receive the same bonus figure because the calculation ceiling applies to both. Use the free EZHRM Bonus Calculator to enter your employee’s actual salary and applicable minimum wage — it runs this calculation instantly. Find it alongside our full suite of free HR calculators for Indian payroll.

The Rs. 7,000 vs Minimum Wage Trap — And Why Most HR Managers Get This Wrong

This is the single most commonly misunderstood part of the Act. Section 12 states that if the salary drawn by an employee is more than Rs. 7,000 per month (or the minimum wage notified for the lowest grade in the scheduled employment), the bonus is calculated on Rs. 7,000 or the minimum wage — whichever is higher.

The 2015 Amendment added “minimum wage for the lowest grade” as an alternative benchmark. This means if your state’s minimum wage for unskilled workers in your industry is, say, Rs. 9,500/month, you cannot cap the bonus calculation at Rs. 7,000. You must use Rs. 9,500 as the calculation base.

Labour department inspections in Tamil Nadu and Karnataka have specifically flagged establishments that used Rs. 7,000 flat when the applicable minimum wage was higher. The underpayment results in arrears plus interest.

How to check: Look up your state’s minimum wage notification for the relevant trade/industry category. You can reference the Labour Ministry’s notification page.

Bonus Percentage — Minimum 8.33%, Maximum 20%: What Determines Your Rate?

The Act sets a floor of 8.33% and a ceiling of 20%. Where you land between those two numbers depends on the company’s “allocable surplus” — a specific financial calculation under Sections 5 and 6 of the Act. In simple terms: the allocable surplus is 67% (for non-banking, non-insurance companies) of the gross profit for the accounting year. If your allocable surplus, when divided among eligible employees, yields more than 8.33%, you are required to pay more — up to 20%.

Most SMEs with tight margins end up at the minimum 8.33%. If you declare a higher percentage in any year as a goodwill gesture, it does not lock you into that for future years. Make it clear to employees — and document it in writing — whether extra payment above 8.33% is “bonus under the Act” or “ex-gratia.”

You can explore related payroll components using the CTC Salary Calculator to understand how bonus fits into the overall compensation structure, and the Full and Final Settlement Calculator for employees who leave mid-year before bonus is paid.

Bonus for Mid-Year Joiners and Leavers

This is another area where HR teams frequently make errors — especially during F and F settlements.

For mid-year joiners: If an employee joins in September 2025 and works through March 2026, they are eligible for bonus on a pro-rated basis — as long as they have completed 30 working days. The formula applies their working days as a proportion of total working days in the accounting year.

For employees who resign before November 30: They are still entitled to their bonus for FY 2025-26. The bonus cannot be withheld simply because they resigned — this is illegal under Section 19 of the Act. Use the Full and Final Settlement Calculator to compute all dues accurately.

For employees terminated for misconduct: Under Section 9, the employer can forfeit bonus for the accounting year in which the dismissal occurred. However, this requires a formal, documented termination for misconduct — not merely a performance issue.

What HR Managers Get Wrong About Statutory Bonus

Here are the six mistakes Indian HR managers make most often:

- Using Rs. 7,000 flat as the calculation base when state minimum wage is higher. Always check your state’s minimum wage for the relevant industry category.

- Treating festival bonuses as “in lieu of” statutory bonus. Unless the festival bonus is explicitly higher than the statutory obligation and declared as such in writing, it cannot substitute for statutory bonus.

- Not paying bonus to probationers. If a probationer earns under Rs. 21,000/month and has worked 30+ days, they are eligible. Probation status is irrelevant to the Act.

- Calculating bonus on full CTC instead of Basic + DA. Only Basic salary and Dearness Allowance count. HRA, conveyance, and special allowances are excluded from both the eligibility ceiling and the calculation base.

- Missing the November 30 deadline. Late payment beyond the 8-month window attracts simple interest at 10% per annum and potential prosecution under Section 28 of the Act.

- Not filing Form D. Many companies pay the bonus but forget to submit the annual return. Form D must be filed within 30 days of making the bonus payment, with your jurisdictional Labour Inspector.

Filing Requirements Under the Payment of Bonus Act

The Act requires employers to maintain four registers and submit one annual return. Form A covers the computation of allocable surplus (kept on file, produced during inspections). Form B is a running register tracking set-on and set-off of allocable surplus across years. Form C records employee-wise details of bonus due, deductions, and actual bonus paid. Form D is the annual return submitted to the Inspector within 30 days of paying the bonus.

EZHRM’s compliance management module tracks these deadlines automatically and flags when Form D is due, so nothing falls through the cracks during the busy Q3 period.

Using the EZHRM Statutory Bonus Calculator

The EZHRM Statutory Bonus Calculator is free, requires no login, and does the heavy lifting in under 60 seconds. Enter the employee’s monthly Basic + DA, the applicable state minimum wage for the lowest grade in your industry, the number of working days completed in the accounting year, and the bonus percentage (8.33% to 20%). The calculator outputs the exact bonus payable, with a breakup showing the calculation ceiling used.

You can also run calculations for your full team using the free HR calculators hub alongside the Leave Encashment Calculator and Notice Period Recovery Calculator to complete your year-end payroll processing in one sitting.

For teams running payroll on EZHRM, the platform auto-computes eligible bonus amounts using your payroll data — no manual entry needed. See how EZHRM handles payroll compliance end-to-end.

Frequently Asked Questions

Is statutory bonus taxable for employees?

Yes. Statutory bonus is treated as income from salary and is fully taxable in the hands of the employee under Section 17(1) of the Income Tax Act, 1961. There is no exemption for bonus received from a private sector employer. It should appear in the employee’s Form 16 under “Salary” and must be included in TDS calculations for the relevant financial year.

Can a company pay less than 8.33% if it makes a loss?

Technically, yes — under the “set-off” provisions, if the allocable surplus is zero or negative, the minimum bonus of 8.33% can be deferred and set off against future surplus years. However, once the company returns to profitability, the deferred amount must be paid. In practice, most SME employers simply pay the minimum 8.33% every year to avoid legal complications and employee grievances.

Does statutory bonus apply to contract workers and third-party staff?

The principal employer is not directly liable for bonus to contract workers — that obligation rests with the contractor. However, if the contractor fails to pay, the principal employer can be held liable under certain interpretations of the Contract Labour Act. Always include a bonus compliance clause in your contractor agreements and verify payment through Form C.

What happens if we pay a festival (Diwali) bonus? Does it count?

A festival bonus can be adjusted against the statutory bonus only if: (a) it is paid in the same accounting year, and (b) the amount equals or exceeds the statutory obligation. If you paid Rs. 4,000 as Diwali bonus and the statutory obligation is Rs. 6,997, you still owe the employee Rs. 2,997 as statutory bonus before November 30. Document festival bonus payments clearly to avoid double-counting disputes during audits.

Our employee resigned in August. Do we still owe them bonus for FY 2025-26?

Yes, if they worked 30+ days in FY 2025-26 (April 2025 to March 2026) and earned under Rs. 21,000/month in Basic + DA. Their entitlement is pro-rated based on working days. The bonus is payable by November 30, 2026 at the latest — it cannot be withheld simply because they resigned.

How do we handle bonus for employees who were on long leave during the year?

Days of authorised leave, maternity leave, lay-off periods, and legal strikes are all counted as “working days” under the Payment of Bonus Act. So an employee on 60-day maternity leave is not disadvantaged. Unauthorised absence is generally excluded from the working days count. Verify your leave records in your leave management system before finalising bonus calculations.

Calculating statutory bonus correctly is not complicated once you know the two ceilings, the minimum wage cross-check, and the November 30 deadline. If your team manages 20+ employees across different salary bands and joining dates, the EZHRM Statutory Bonus Calculator will save you an afternoon of spreadsheet work — and help you catch the minimum wage error before a labour inspector does. For more payroll guides, visit the EZHRM HR and Payroll blog.