PF and ESI Calculation India 2026: Rates, Formula & HR Guide

It’s the 12th of the month. Your accounts team just pasted a salary sheet with 47 employees — some above ₹21,000 gross, some below. Your payroll software threw an error on three records. And someone in finance is asking why your “total cost to company” numbers don’t match the offer letters from six months ago. Sound familiar? Nine times out of ten, the root cause is a PF or ESI calculation gone wrong.

PF and ESI are the two most common statutory deductions in Indian payroll — and also the two most commonly miscalculated. This guide walks you through exactly how the numbers work in 2026, with real formulas, worked examples, and the mistakes you want to avoid before EPFO or ESIC comes knocking.

- PF: Employee pays 12% of Basic+DA; Employer pays 12% split into 3.67% (EPF) + 8.33% (EPS pension). Mandatory only up to ₹15,000 Basic+DA.

- ESI: Employee pays 0.75% and Employer pays 3.25% of gross salary. Applies only when gross salary ≤ ₹21,000/month.

- ECR challan must be filed and paid by the 15th of the following month — both PF and ESI.

- Use EZHRM’s free PF & ESI Calculator to get the exact breakdown in seconds.

What Are PF and ESI? (And Why Both Matter)

PF (Provident Fund) and ESI (Employees’ State Insurance) are mandatory social security contributions governed by two separate Central Acts — the Employees’ Provident Funds and Miscellaneous Provisions Act, 1952 and the Employees’ State Insurance Act, 1948 respectively. Both are administered by autonomous bodies: EPFO handles PF, and ESIC handles ESI.

Think of PF as long-term retirement savings with a forced contribution from both sides. ESI is health and disability insurance — employees covered under ESI get access to ESIC hospitals, maternity benefits, and disability allowance without any out-of-pocket expense. For your workers earning under ₹21,000, ESI is often their only real health cover.

PF applies to establishments with 20 or more employees. ESI applies to factories and specified establishments with 10 or more employees in ESI-notified areas. Once an establishment crosses either threshold, coverage is mandatory and irrevocable even if headcount later falls below.

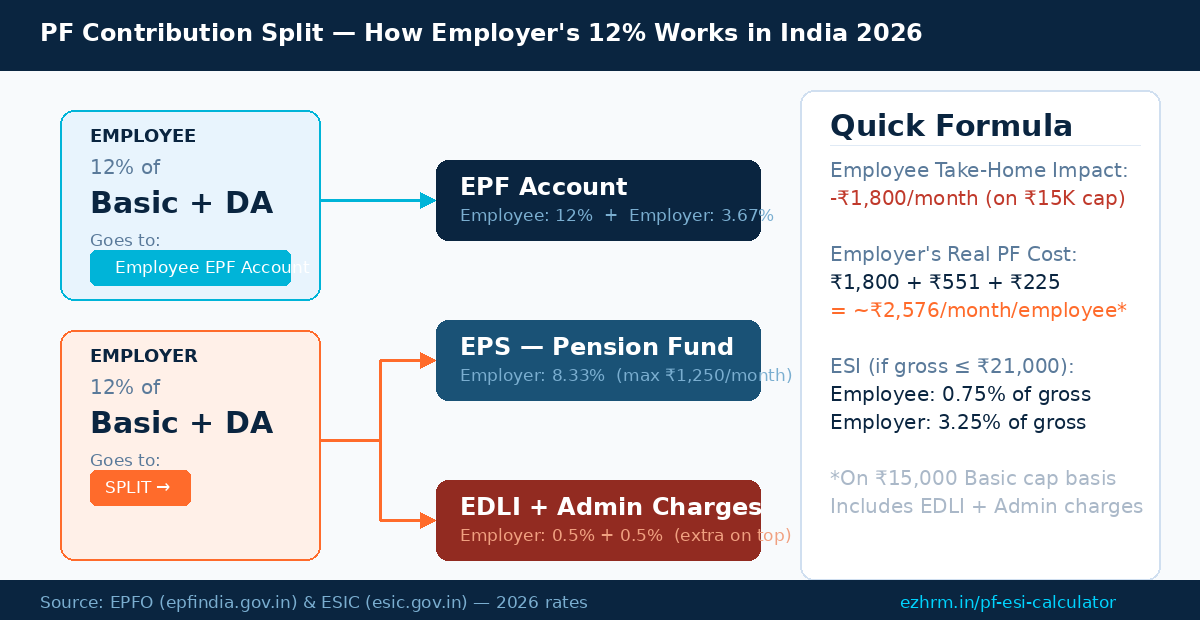

PF Contribution Rates and Formula in 2026

The PF contribution rate has been 12% for both employee and employer since 1952 — and it hasn’t changed. What confuses most HR managers is how the employer’s 12% gets split.

Employee’s Contribution

The employee contributes 12% of Basic Salary + Dearness Allowance (DA) to their EPF account. This entire 12% goes into the employee’s EPF account and earns the EPFO-declared interest (8.25% for FY 2023-24, subject to annual revision).

If Basic + DA exceeds ₹15,000, mandatory deduction is still calculated only on ₹15,000 unless the employee opts for voluntary higher contribution. A new joiner with Basic ₹25,000 will still have PF deducted on ₹15,000 (i.e., ₹1,800) unless they request voluntary PF on actual basic.

Employer’s 12% Split: EPF + EPS

The employer’s 12% does NOT all go into the employee’s EPF balance. It splits as follows:

- 3.67% → Employee’s EPF account (retirement corpus)

- 8.33% → EPS — Employees’ Pension Scheme (capped at ₹1,250/month, i.e., 8.33% of ₹15,000)

This is a critical point many employees don’t understand. Their “PF balance” shown in the EPFO passbook only includes the employee’s 12% plus the employer’s 3.67%. The 8.33% goes to the pension fund — they’ll see that as a monthly pension after retirement, not as a lump sum.

EDLI and Admin Charges (Employer Only)

On top of the 12%, employers pay two additional amounts:

- EDLI (Employees’ Deposit Linked Insurance): 0.5% of Basic+DA, capped at ₹75/month per employee. This funds life insurance for covered employees.

- EPF Admin Charges: 0.5% of Basic+DA, minimum ₹500/month per establishment.

So the actual total employer outgo on PF is roughly 13% of the capped Basic+DA (12% + 0.5% EDLI + 0.5% admin). Use the free EZHRM PF Calculator to see this broken out clearly for any salary — it shows EPF, EPS, EDLI, and total cost in one click.

ESI Contribution Rates and Formula in 2026

ESI is simpler than PF in one respect: it’s calculated on gross salary, not just basic. The rates effective since 1 July 2019 — and unchanged in 2026 — are:

- Employee contribution: 0.75% of gross salary

- Employer contribution: 3.25% of gross salary

Who Qualifies for ESI?

ESI applies to employees whose gross salary is ₹21,000/month or less (₹25,000 for persons with disability). One important nuance: if an employee’s gross crosses ₹21,000 mid-year, ESI deductions continue for the rest of that contribution period (Apr–Sep or Oct–Mar). They don’t stop immediately.

Employees getting a daily average wage of ₹176 or less are exempt from the employee-side contribution, but the employer still has to pay their 3.25%.

ESI Calculation Example

Employee gross salary: ₹18,000/month

- Employee ESI: 0.75% × ₹18,000 = ₹135

- Employer ESI: 3.25% × ₹18,000 = ₹585

- Total monthly ESI outgo: ₹720

For a 50-person workforce where 30 employees earn under ₹21,000, your monthly ESI outgo as an employer could easily cross ₹15,000–₹18,000. Run the numbers quickly with the EZHRM PF & ESI Calculator before you finalise your monthly payroll cost sheet.

Complete PF and ESI Calculation: Side-by-Side Examples

Here are three typical employee profiles and their exact deductions:

| Component | Employee A Basic ₹12,000 / Gross ₹18,000 |

Employee B Basic ₹18,000 / Gross ₹28,000 |

Employee C Basic ₹30,000 / Gross ₹45,000 |

|---|---|---|---|

| PF Eligible Basic | ₹12,000 | ₹15,000 (capped) | ₹15,000 (capped) |

| Employee PF (12%) | ₹1,440 | ₹1,800 | ₹1,800 |

| Employer EPF (3.67%) | ₹440 | ₹551 | ₹551 |

| Employer EPS (8.33%) | ₹1,000 | ₹1,250 | ₹1,250 |

| ESI Applicable? | Yes (gross ≤ ₹21K) | No (gross > ₹21K) | No (gross > ₹21K) |

| Employee ESI (0.75%) | ₹135 | — | — |

| Employer ESI (3.25%) | ₹585 | — | — |

| Total Employee Deductions | ₹1,575 | ₹1,800 | ₹1,800 |

| Total Employer Statutory Cost | ₹2,025 | ₹1,801 | ₹1,801 |

Note: EDLI (0.5%) and admin charges (0.5%) are excluded from this table for readability. Include them for true CTC costing.

For automatic breakdowns like this across your entire headcount, EZHRM’s payroll software handles it in real time — no manual tables needed. You can also explore the full range of free HR calculators on the EZHRM tools hub.

ECR Filing: Deadlines and How It Works

Both PF and ESI challans must be filed and paid by the 15th of the following month. If the 15th falls on a Sunday or bank holiday, the deadline moves to the next working day.

For PF, you file the Electronic Challan cum Return (ECR) on the EPFO Unified Portal. The ECR captures each employee’s UAN, gross wages, EPF wages, EPS wages, and contribution amounts. After ECR submission, you generate the challan and pay through net banking.

For ESI, you file online through the ESIC portal. ESI has two contribution periods:

- April to September — contribution and returns

- October to March — contribution and returns

Missing the 15th deadline attracts damages at 12% per annum for PF and 12% simple interest for ESI plus additional penalties. It’s not a gentle nudge — EPFO has been actively issuing demand notices to SMEs since 2024. Set calendar reminders or let your compliance management system handle the alerts automatically.

What HR Managers Get Wrong About PF and ESI

These are the mistakes I’ve seen come up repeatedly across SMEs — and every single one is avoidable.

- Calculating ESI on basic instead of gross. ESI uses gross salary (all earnings except OT allowance and washing allowance). Using basic gives a wrong, lower figure that can trigger demands in an ESIC inspection.

- Not continuing ESI after salary crosses ₹21,000 mid-year. If your employee gets a hike in June, ESI continues until 30 September — the end of that contribution period. Stopping immediately is non-compliant.

- Not capping EPS at ₹1,250. Employer EPS is always capped at 8.33% of ₹15,000 = ₹1,250, regardless of actual basic salary. Some HR managers calculate 8.33% on ₹25,000 or ₹30,000 and overpay the pension fund.

- Missing EDLI and admin charges in CTC letters. The offer letter says “CTC ₹5,00,000” but the HR team forgot to include EDLI and admin charges when building the CTC. Employees get a nasty surprise, and finance gets a budget variance.

- Treating voluntary PF as mandatory. If an employee requests voluntary PF on actual basic (say, ₹30,000), that’s their choice — not a statutory mandate. The employer’s corresponding contribution can also remain capped at ₹15,000 basis unless you have a policy to match.

- Forgetting the ₹176/day ESI exemption for low-wage workers. Daily-wage workers earning ₹176 or less are exempt from the employee’s 0.75% contribution. You still pay the employer’s 3.25%. Getting this wrong means either under-deducting or over-deducting from vulnerable workers.

Also worth checking: did you correctly link Full & Final Settlement calculations to PF and ESI? The last month’s PF/ESI must still be deposited even after an employee exits — this is where many F&F settlements get delayed.

PF vs ESI: Quick Comparison

| Criteria | PF (EPFO) | ESI (ESIC) |

|---|---|---|

| Governing Act | EPF & MP Act, 1952 | ESI Act, 1948 |

| Applicability threshold | 20+ employees | 10+ employees (ESI areas) |

| Wage ceiling | ₹15,000 Basic+DA (mandatory) | ₹21,000 gross/month |

| Employee rate | 12% of Basic+DA | 0.75% of gross |

| Employer rate | 12% + 0.5% EDLI + 0.5% admin | 3.25% of gross |

| Filing deadline | 15th of next month (ECR) | 15th of next month |

| Benefit to employee | Retirement corpus + pension | Medical, maternity, disability |

You can also cross-check your salary structures against the CTC Salary Calculator and the Gratuity Calculator to ensure your total employer cost projections are accurate before sending out offer letters.

Frequently Asked Questions

Is PF mandatory if basic salary exceeds ₹15,000?

For employees who were already PF members before their salary crossed ₹15,000, yes — PF contribution continues on actual basic unless they opt out under the International Workers exemption. For new hires joining with basic above ₹15,000, enrollment is optional but mandatory if they were previously covered. Most companies simply keep it mandatory for simplicity and compliance safety.

Can an employer pay PF on actual basic instead of capping at ₹15,000?

Yes, voluntarily. This is called “uncapped PF.” The employer then contributes 3.67% on actual basic (EPS still stays capped at ₹1,250). This increases the employer’s PF outgo and the employee’s retirement corpus, but also reduces take-home pay. Many IT and manufacturing companies offer this as a benefit — it needs to be clearly stated in the appointment letter.

What happens if you miss the 15th deadline for PF/ESI payment?

EPFO charges damages at 5%–25% of the unpaid amount depending on delay period, plus 12% per annum simple interest. ESIC charges 12% simple interest per annum. Repeated defaults can trigger inspections and prosecution under the respective Acts. Set automated reminders or use a compliance management tool to never miss a date.

Does ESI apply to contractors and contractual workers?

Yes. Under the ESI Act, the principal employer is responsible for ESI contributions of contract workers deployed at their premises. If the contractor fails to pay, the principal employer is liable. Always verify that your contractor’s manpower bills include ESI, and maintain records to prove compliance in case of an ESIC inspection.

Is the PF contribution paid on gross salary or basic?

PF is calculated on Basic + DA only — not gross salary. ESI is calculated on gross salary. This is the most common source of confusion in payroll. Allowances like HRA, conveyance, and special allowance are excluded from the PF base but are included in the ESI gross. Use EZHRM’s free PF & ESI Calculator to instantly verify both figures side by side.

Can an employee opt out of ESI?

No. ESI is mandatory for eligible employees (gross ≤ ₹21,000). Neither employer nor employee can waive it. The only exception is employees already covered under another approved medical scheme with equivalent benefits — this requires a specific exemption notification from ESIC, which is rarely granted. In practice, if the salary is below the ceiling and the establishment is covered, ESI must be deducted.

If you’re spending more than 30 minutes per month cross-checking PF and ESI figures manually, that’s time worth getting back. Run any salary through EZHRM’s free PF & ESI Calculator for an instant, accurate breakdown — and explore the rest of the free HR calculators to cover your full payroll compliance checklist. For more HR guides like this one, head to the EZHRM blog.