Your company just opened a second office in Pune. You’re based in Gurugram. Your payroll team — sharp as they are — runs the first Pune payroll exactly the same way they run the Haryana payroll. No Professional Tax deducted. Why would they? Haryana doesn’t have PT. Six months later, a Maharashtra PT authority notice lands on the MD’s desk. The penalty? ₹4,800 in interest and a ₹5,000 late registration fine. That’s a bad Monday morning.

Professional tax on salary is one of those compliance items where the rules are state-specific, the amounts are small, and the cost of getting it wrong is disproportionately painful. This guide walks you through the full employer compliance picture — registration, deductions, return filing, multi-state rules, and the mistakes that generate notices.

TL;DR — Professional Tax on Salary India 2026

- Professional Tax (PT) is a state-level tax on salaried income, capped at ₹2,500/year under Article 276 of the Constitution

- Employers must register for an Enrolment Certificate (EC) and/or Registration Certificate (RC) before the first salary run in any PT state

- PT is calculated on monthly gross salary (not CTC, not basic) using the applicable state slab — use the EZHRM Professional Tax Calculator to get the right number instantly

- PT paid by employees is fully deductible under Section 16(iii) of the Income Tax Act — available under both old and new tax regimes in FY 2026-27

What Is Professional Tax on Salary?

Professional tax on salary is a tax levied by state governments on income earned from employment, professions, trades, and callings. The constitutional authority is Entry 60 of List II (State List) and Article 276 of the Constitution of India, which sets a hard ceiling of ₹2,500 per year as the maximum PT any individual can be charged.

In practice, your role as an employer has two parts: (1) deduct the correct PT from each employee’s monthly gross salary based on the applicable state slab, and (2) deposit that amount with the state PT authority by the prescribed deadline. The employer also pays a small annual PT (Enrolment Certificate fee) out of its own pocket — this is a company expense, not recoverable from employees.

To see how PT fits into the complete salary picture alongside PF, ESI, and TDS, run your numbers through our CTC to In-Hand Salary Calculator — it accounts for all deductions and shows you exactly what reaches the employee’s bank account.

Which States Have Professional Tax — and Which Don’t?

PT is levied by approximately 16 Indian states and union territories. The absence of PT in some of India’s largest employment hubs — Delhi, Haryana, Uttar Pradesh, Rajasthan — means many HR managers working out of the NCR have never had to deal with it. That changes the moment your company opens an office or factory in Maharashtra, Karnataka, or West Bengal.

| State / UT | PT Applicable? | Max Annual PT | Governing Act |

|---|---|---|---|

| Maharashtra | ✅ Yes | ₹2,500 | Maharashtra State Tax on Professions Act 1975 |

| Karnataka | ✅ Yes | ₹2,400 | Karnataka Tax on Professions Act 1976 |

| West Bengal | ✅ Yes | ₹2,500 | West Bengal State Tax on Professions Act 1979 |

| Andhra Pradesh | ✅ Yes | ₹2,400 | AP Tax on Professions, Trades Act 1987 |

| Telangana | ✅ Yes | ₹2,400 | Telangana Tax on Professions Act |

| Gujarat | ✅ Yes | ₹2,400 | Gujarat Panchayat, Municipal, Professions Tax Act 1976 |

| Madhya Pradesh | ✅ Yes | ₹2,500 | MP Vritti Kar Adhiniyam 1995 |

| Tamil Nadu | ✅ Nominal | ₹1,200 | Tamil Nadu Municipal Laws (Amendment) Act |

| Kerala | ✅ Nominal | ₹1,200 | Kerala Municipal Act |

| Assam | ✅ Yes | ₹2,400 | Assam Professions, Trades Act 1947 |

| Delhi | ❌ No | — | — |

| Haryana | ❌ No | — | — |

| Uttar Pradesh | ❌ No | — | — |

| Rajasthan | ❌ No | — | — |

The rule that trips up multi-state employers: PT applicability is determined by the state where the employer has a registered establishment — not where the employee physically works. If your employee works remotely from home in Hyderabad but is on the rolls of your Bengaluru office, Karnataka PT applies, not Telangana.

How to Calculate Professional Tax on Salary — Step by Step

Professional tax is calculated on monthly gross salary. Not basic pay, not CTC, not net pay — monthly gross. Gross salary here means the sum of all monthly fixed salary components: basic, HRA, special allowance, and other regular monthly allowances. It generally excludes one-time payments like arrears, performance bonuses, and expense reimbursements.

PT Calculation: Worked Examples

| Employee | State | Monthly Gross | Monthly PT | Annual PT |

|---|---|---|---|---|

| Rahul (Software Engineer) | Karnataka | ₹72,000 | ₹200 | ₹2,400 |

| Priya (HR Manager) | Maharashtra | ₹55,000 | ₹200 (₹300 in Feb) | ₹2,500 |

| Sumit (Junior Accountant) | West Bengal | ₹12,000 | ₹110 | ₹1,320 |

| Deepa (Sales Executive) | Gujarat | ₹28,000 | ₹200 | ₹2,400 |

| Anita (Customer Support) | Karnataka | ₹13,500 | ₹150 | ₹1,800 |

| Vikram (IT Analyst) | Delhi | ₹90,000 | ₹0 | ₹0 |

Rather than looking up state slabs manually every month, use the free EZHRM Professional Tax Calculator — enter the gross salary, select the state, and get the correct monthly and annual PT instantly. It covers all major states and is updated for FY 2026-27.

Maharashtra’s February ₹300 quirk: Maharashtra employees earning above ₹10,000/month are deducted ₹200 in 11 months and ₹300 in February, totalling ₹2,500/year. This is the most commonly missed payroll adjustment in Maharashtra payroll runs.

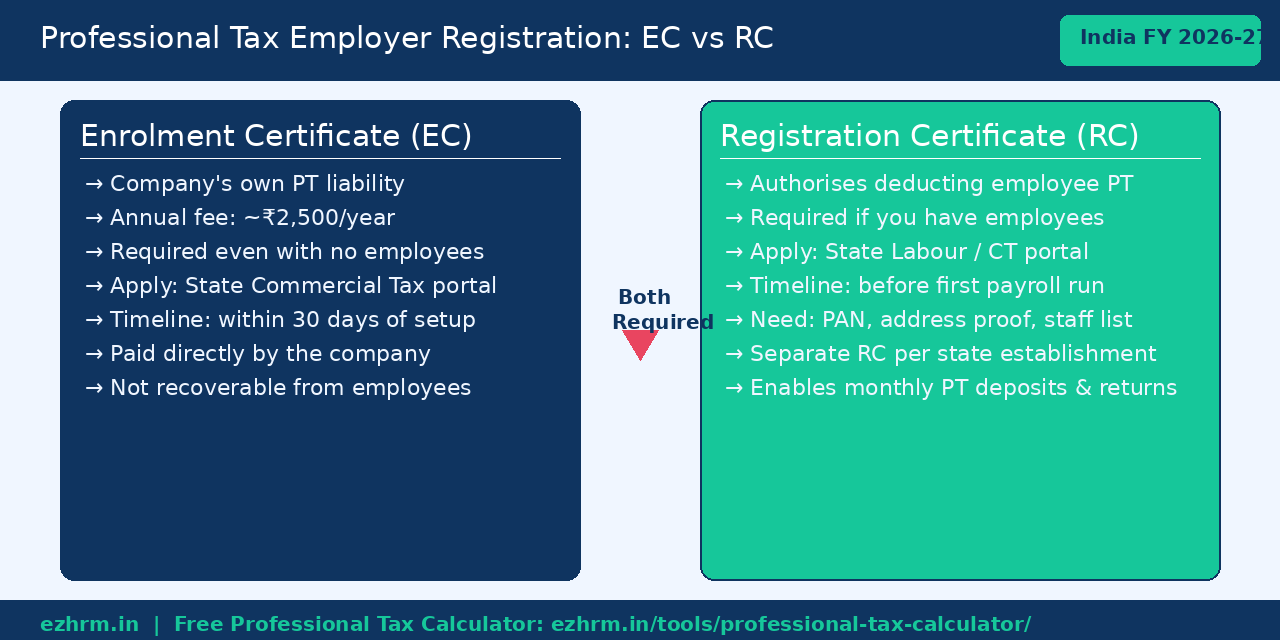

Employer Registration for Professional Tax: EC vs RC

Before you run a single payroll in a PT state, your company needs to be registered with the state PT authority. Most states require two distinct certificates:

Enrolment Certificate (EC)

The EC covers the employer’s own PT liability — the annual fee the company pays for carrying on its business or profession. This is typically ₹2,500 per year, paid directly by the company. Every establishment in a PT state needs an EC, regardless of whether it has employees.

Registration Certificate (RC)

The RC authorises you to deduct PT from employee salaries and remit it to the government. If you have employees in a PT state, you need an RC. The RC application typically requires: the company’s PAN, establishment address proof, list of employees with salary details, and authorised signatory details. Most states now offer online RC registration through their commercial tax or labour department portals.

Registration timelines: Most states require registration within 30 days of starting operations or employment in that state. Some states (Karnataka, Maharashtra) have penalties specifically for late EC/RC registration — separate from late deposit penalties. Don’t wait for the first payroll to initiate registration.

PT Return Filing: Deadlines & Formats by State

Collecting PT from employee salaries is only half the job. You must also deposit it with the state authority and file periodic returns. Missing these deadlines is where most compliance failures happen.

| State | Deposit Frequency | Deposit Deadline | Annual Return |

|---|---|---|---|

| Maharashtra | Monthly | Last day of the following month | 30 June each year |

| Karnataka | Monthly | 20th of the following month | 60 days from year-end |

| West Bengal | Monthly / Quarterly | 21st of following month / quarter | 30 June each year |

| Gujarat | Monthly | 15th of the following month | With final monthly return |

| Andhra Pradesh / Telangana | Monthly | 10th of the following month | Form IV by 30 June |

| Madhya Pradesh | Monthly | Last day of the following month | Annual return Form 7 |

Penalties for late deposit: interest at 1.25–2% per month on the outstanding amount, plus late filing penalties ranging from ₹250 to ₹5,000 depending on the state and duration of default. For a 50-employee company in Maharashtra missing 2 months of PT, the interest alone could exceed the actual PT collected. The compliance cost far outweighs the original tax.

EZHRM’s statutory compliance module tracks PT deposit and return deadlines across all your registered states and sends automated reminders before due dates — so your payroll team doesn’t have to maintain separate state-wise calendars.

PT on Contract Workers, Trainees, and Part-time Employees

One area where HR managers often lack clarity is PT applicability for non-permanent workforce arrangements. Here’s the practical guidance:

Fixed-term contract employees: PT applies in the same way as permanent employees. Calculate PT on monthly gross salary using the state slab. For the month of joining or separation, calculate PT on the actual salary paid (prorated). Our Full & Final Settlement Calculator handles PT for the exit month correctly alongside other F&F components.

Trainees and apprentices: PT applicability depends on the state. In Maharashtra, trainees and apprentices under the Apprentices Act 1961 are generally exempt. In Karnataka, they are subject to PT if the stipend crosses the slab threshold. Always verify the specific state notification.

Part-time employees: PT applies on the salary actually paid. A part-time employee earning ₹7,000/month in Karnataka pays nil PT (below ₹9,999 threshold). The same person earning ₹11,000/month would attract ₹100 PT.

Independent contractors and consultants: PT technically applies to professionals in their individual capacity under the “professions” arm of the respective state Acts. However, when you pay a consultant a professional fee, you are generally not required to deduct PT as an employer — the consultant is responsible for their own PT registration and payment. This is a common area of confusion. If in doubt, check the specific state Act.

Professional Tax vs Income Tax: The Section 16(iii) Benefit

PT is not a form of double taxation. It is a state levy, while income tax is a central government levy — both exist independently. What makes PT relatively painless from an employee perspective is that the full PT paid during the year is deductible from gross salary under Section 16(iii) of the Income Tax Act when computing taxable income.

This deduction is available under both the old and the new tax regime for FY 2026-27. Unlike most deductions (80C, HRA, LTA) that are disallowed under the new regime, the Section 16(iii) PT deduction survives. An employee in Maharashtra earning above ₹10,000/month saves ₹750 in income tax (at the 30% slab) because of the ₹2,500 PT deduction — a small but real benefit.

For a full breakdown of how PT, PF, ESI, and TDS interact to determine actual take-home, use our suite of free HR calculators — including the Professional Tax Calculator, PF & ESI Calculator, and Overtime Calculator.

What HR Managers Get Wrong About Professional Tax Compliance

1. Applying the same PT to all states. Running ₹200 flat for every employee regardless of state — or worse, applying no PT for a state that levies it — is the most common error. PT is state-specific. Multi-state payroll requires state-wise configuration.

2. Delaying EC/RC registration. Many companies start operations in a new state, run payroll for a few months, and only then think about PT registration. By then, you’re already non-compliant. Registration must happen before the first payroll run.

3. Calculating PT on basic pay, not gross salary. Professional Tax slabs are based on monthly gross salary. Using basic pay will under-deduct PT for mid-to-senior level employees, creating a shortfall that must eventually be made up.

4. Missing the Maharashtra February adjustment. Maharashtra’s ₹300 February PT deduction catches HR teams off guard every year. If your payroll software is configured for ₹200 flat, you’ll under-deduct by ₹100 in February — creating a cumulative liability.

5. Including reimbursements in PT salary base. Expense reimbursements (conveyance, fuel, mobile) are not salary — they shouldn’t form part of the gross salary used to determine the PT slab. Including them inflates the slab and leads to over-deduction, which then needs to be rectified.

6. Not tracking PT for remote workers on a different state’s rolls. With hybrid work now the norm, many employees work physically from a different state than where their employer is registered. PT follows the employer’s registration state — not the employee’s physical location. Get this mapping right in your HRIS before each payroll run.

Frequently Asked Questions — Professional Tax Compliance India 2026

How many days does an employer have to deposit PT after deduction?

It depends on the state. Maharashtra allows until the last day of the month following deduction. Karnataka requires deposit by the 20th of the following month. Andhra Pradesh and Telangana require deposit by the 10th. Always follow your specific state’s PT Act — missing even one month’s deadline can trigger interest at 1.25–2% per month on the overdue amount.

Does a company need to register for PT in every state where it has employees?

Yes — if that state levies PT, your establishment in that state must obtain an Enrolment Certificate (EC) and a Registration Certificate (RC) before the first payroll run. Each branch or registered establishment needs its own RC in most states. Operating without registration while deducting PT is itself a compliance violation.

What is the penalty for not deducting Professional Tax from employee salaries?

Penalties vary by state. Maharashtra imposes interest at 1.25% per month on unpaid PT plus a minimum penalty of ₹5,000 for wilful non-compliance. Karnataka’s Act allows for prosecution in cases of persistent default. West Bengal can impose penalties up to the amount of tax due. Beyond the financial cost, repeat non-compliance can lead to the state PT authority attaching company bank accounts for recovery.

Is Professional Tax applicable on salary paid during notice period?

Yes. PT applies on all salary paid during the employment relationship, including the notice period. In the final month of employment (F&F month), PT is calculated on the salary actually paid — which may be prorated if the employee exits mid-month. Use our Full & Final Settlement Calculator to handle the exit month correctly alongside notice period recovery and earned leave encashment.

Can an employee claim a refund if excess PT was deducted?

Yes, but the process differs by state. Most states allow the employer to adjust the over-deduction in the following month’s payroll within the same financial year. After year-end, the employee must file an application with the state PT authority for a formal refund — which is procedurally slow. Best practice: reconcile PT monthly and correct over-deductions before year-end rather than pursuing refunds after.

Is there a central Professional Tax Act in India?

No. There is no single central Professional Tax Act. Each state that levies PT has its own legislation — Maharashtra’s Professions Tax Act 1975, Karnataka’s Tax on Professions Act 1976, West Bengal’s State Tax on Professions Act 1979, and so on. This is why PT slabs, deadlines, and penalty provisions differ across states. Always refer to the specific state Act applicable to your establishment.

For more compliance guides like this, visit the EZHRM HR & Payroll blog. And whenever you need to verify a PT amount quickly — for any employee in any state — the EZHRM Professional Tax Calculator is the fastest way to get it right without digging through state government websites. If your team processes payroll for 20+ employees across multiple states, EZHRM’s payroll software handles PT deductions, deposits, and return tracking automatically — so professional tax compliance is one less thing on your to-do list.